The Australian sheep market in 2026 hasn’t looked like this in close to a decade.

Mutton, lamb and wool are all running strong at the same time. That’s not something most producers have seen in a long while, and it’s worth understanding what’s driving it and what it means practically for your business.

What the Australian sheep market looks like right now

Mutton: the market no one expected

For years, mutton sat at the bottom of the pricing ladder. Processors used the mutton chain to fill capacity, and prices reflected that reality.

That’s shifted significantly. Sheep slaughter nationally is down 9% year to date compared to the same period in 2025, and that tighter supply is pushing prices higher week on week. The National Mutton Indicator hit a record high of 889c/kg this week, with some saleyards reporting up to $10/kg dressed weight. Processors that traditionally focused on lamb have switched significant capacity to mutton chains, chasing strong export demand.

Restocker demand is adding further upward pressure. Producers who want to rebuild their flocks are competing with processors for the same sheep, and scanned-in ewes are expected to push from $400 to $500 per head in the months ahead.

The floor of the market at the saleyards is sitting around $110 to $115 a head for light sheep. That’s a baseline most producers weren’t seeing 12 months ago.

The National Mutton Indicator has set a record high for the same week of the year, every single week in 2026.

Lamb: record prices, tighter supply ahead

Lamb prices are at historically high levels, trading between $10.50 and $11.50 per kilogram dressed weight.

The reason is straightforward. MLA is forecasting lamb slaughter to fall a further 11% in 2026, following a 6.9% fall in 2025. Several years of heavy turn-off across Victoria, South Australia and southern NSW, combined with difficult seasonal conditions, have reduced the pool of lambs available. Less supply, sustained demand. Prices have responded accordingly.

Early scanning results for this spring are strong, and a larger lamb cohort is expected from September and October. That will bring some relief to supply further down the year. But through the winter months, the current pricing environment is likely to hold.

Wool: the comeback most people didn’t predict

The Australian sheep market for wool has surprised almost everyone.

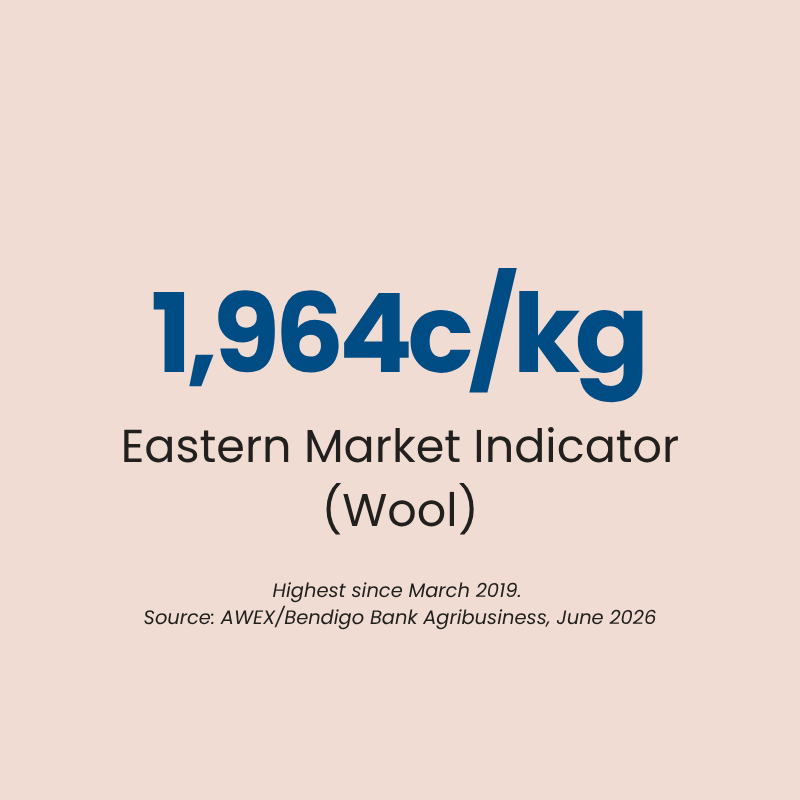

The Eastern Market Indicator is sitting at 1,964c/kg, its highest level since March 2019. It has risen 84 cents in a fortnight, with five consecutive selling days of gains.

Two things are driving it. Nationally, the wool clip has been contracting for years as producers moved away from Merino enterprises or left the industry altogether. Supply is genuinely tighter. And demand from China has returned sharply, with Chinese manufacturers buying aggressively into fine Merino for next-to-skin garments and activewear. Italian spinners and weavers have also been competitive in the rooms.

The combination of tight supply and renewed buyer competition has pushed the market to levels not seen in seven years. The most recent national offering was the smallest in 12 months, and buyer demand held firm regardless. That tells you something about where this market is heading.

What Australian sheep market returns are actually going back into

The strong market figures are real. But for producers across southern Australia, the context matters.

Much of Victoria, South Australia, Tasmania and southern NSW has been through three consecutive below-average seasons. The drought has reduced flock numbers, pushed turn-off higher than any producer would have chosen, and deferred a lot of capital decisions that needed to happen. Input costs, feed costs and labour costs have all climbed in the same period.

The money coming in right now isn’t being pocketed. For most operations, it’s going back into the business. Rebuilding the breeding base. Replenishing reserves. Addressing what was deferred. The national flock is sitting around 67 million head at June 2026, down nearly 3% on last year. A rebuild is expected, but it will be gradual, and it depends heavily on consistent seasonal improvement.

The money coming in right now is going back into the business. Flock rebuild, deferred decisions, getting the infrastructure right for the next cycle.

Building for the next phase

When income improves after a period of sustained pressure, producers think about what they’ve been putting off. For sheep enterprises, that often means shearing sheds that have been operating beyond their useful life, yards that require covering, and hay and grain infrastructure that was deferred because the budget wasn’t there.

The flock rebuild is coming. Scanning results are strong, ewe retention is lifting, and MLA is forecasting the national flock to recover toward 79 million head by 2027. Getting your infrastructure right now, ahead of that growth, is a practical decision. Building into a larger flock is significantly harder than building before it arrives.

Across every category, the Australian sheep market is presenting an opportunity worth acting on. Action Steel has been working with Australian sheep farmers for 25 years, designing and building sheds for their enterprise. Nothing pulled from a shelf.

If you’re thinking about a farm shed build, get in touch and chat to us about your options.

1800 68 78 88

1800 68 78 88  [email protected]

[email protected]